This year I found myself having more discussions with teams at other family offices (“FOs”) about venture capital and how to best invest in the space. My experience in these conversations is there is strong interest by FO teams, or the principals themselves, to begin investing directly in venture capital opportunities. Venture is still a hot topic, despite the negative headlines associated with SoftBank’s misadventures, and we have lots of money. We should do it direct, right?

The typical logic for FOs considering a direct venture strategy is if we commit resources in-house, we can cut out the fees and get similar, or better, outcomes yielding higher net returns. The assumption tends to be we have a smart staff and we can figure this out. We’ve got a big-name family behind us, a large check book, a flexible mandate, and a differentiated time horizon, so it should be easy to get access to the best deals. I wish the playbook were that easy to execute.

Let’s look at expectations FOs might have and dive into what is often the reality of the situation. I’m going to use general assumptions about FOs here, but note that every FO is its own snowflake and generalized circumstances might not apply to that organization. FOs have a long history with venture investing and some have great success with the asset class.

Expectation: We can have one or two people on staff committed part time and succeed.

Reality: A staff member needs to be doing this full time if you want to have a shot at sustainable success. The time commitment can come in conflict with the resources the FO is willing to invest in a venture strategy.

Finding good opportunities, managing deal flow sources, connecting with entrepreneurs, developing relationships with service providers, helping solve problems for your portfolio companies, and being a part of the early-stage community is a full-time job. If the goal is to do true venture style investing, you need to have a good answer about why you can get allocation in a deal that also includes a top tier venture firm operating in the area or sector. Lacking a solid answer should prompt introspection about a viable path to success with the resources allocated to the task. FO principals should put real thought into what assets they’re willing to commit to early stage investing and if the commitment is aligned with the time from staff necessary for a fair shot at success.

Expectation: We will get access to quality deals with our limited efforts.

Reality: Adverse deal selection is a betch. You’ll fund companies you shouldn’t be funding. Building a pipeline of quality partners and ideas takes effort. Decisions will be made based on the relative quality of the deals you do see.

I lived the consequences of having your view about a venture opportunity being anchored to the quality of your pipeline. You wake up a few years later realizing you were an idiot and your standards were too low in part because the team wasn’t seeing enough quality deals, if any. Too bad your team already made a bunch of investments because the team was ‘killing it’ with their proprietary deal flow and now you realize your venture portfolio is more likely to be steaming pile of toxic waste ready to meltdown at any moment than it would be a group of companies comparable to top tier venture portfolios. Managing this type of scenario could entail helping existing companies in non-financial ways while being careful about which businesses are worthy of additional capital and having the team go back to the drawing board with lessons learned to build a true sustainable venture strategy or outsource all venture dollars to funds.

Expectation: We have good taste in businesses and will know a good deal when we see one.

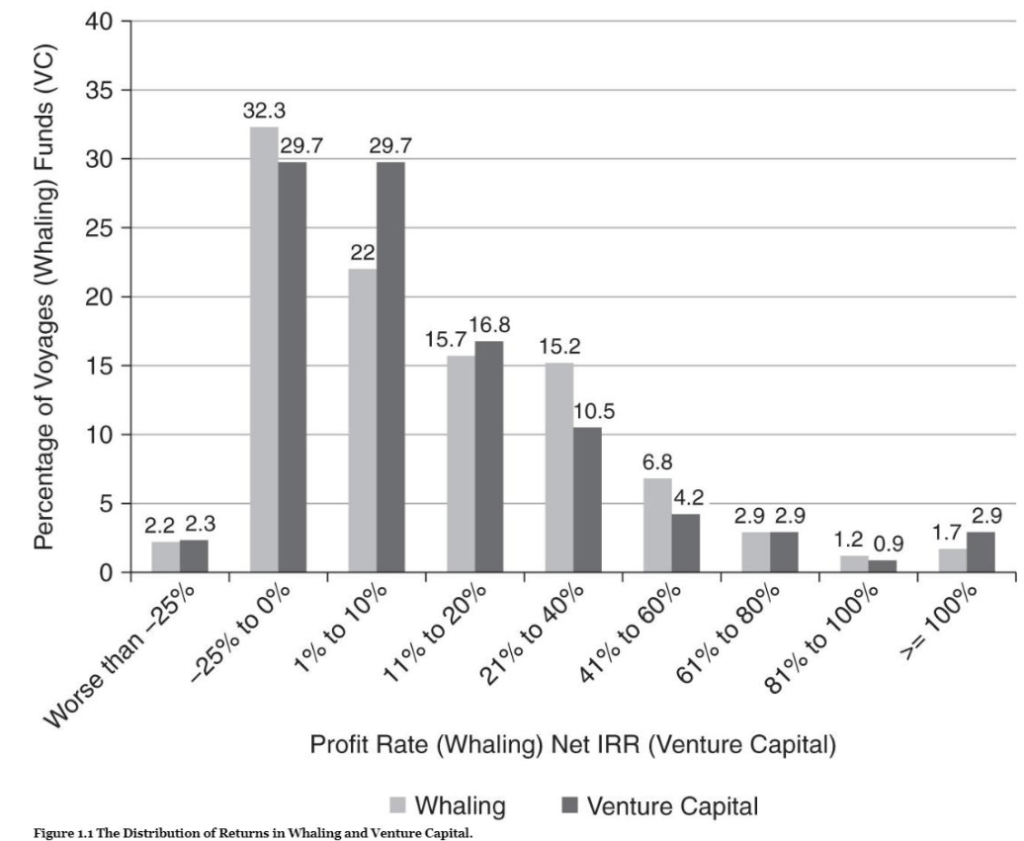

Reality: The mid-level or junior person you have working on venture deals has a PE/public markets/consulting/worked in the business/golf buddy background and doesn’t have a compass that points north in the land of venture capital. Below are two charts, one from Correlation Ventures and one from VC: An American History that give context for what to expect for venture investment outcomes.

I’m surprised about how few conversations FOs have with venture capitalists to help FOs understand diligence, term sheets, returns, etc. for venture opportunities. Some FO teams are more than willing to dive right in. I used to believe underwriting to a 50% IRR was going to be a home run for our team when I first started doing direct early stage deals. Conversations with full-time venture investors made me realize my hurdle of what was expected from a quality venture deal was too low given the failure rate of these businesses. Throw a former PE associate at this problem without any context and they’ll probably think a 50-60% IRR target return will lead to success. Outcomes will likely fall short of expectations.

Understanding what drives failure in venture investments is important when thinking about how you conduct due diligence. My experience is most FOs explore this issue on the surface at best, along with other basic challenges, before deploying capital directly into venture deals. Talking to the person managing capital relationships for an incubator to source deals isn’t enough. Stepping on avoidable land mines is a great way for principals to become disillusioned with the strategy and a huge drag on the team’s time. Not understanding the problems, value creation expectations, and ways the team can help young portfolio companies can be a source of friction, stress, and disappointment.

Expectation: We will be patient and use our resources to connect with good partners to help us ramp up the curve and succeed.

Reality: The team will invest in too many deals too quickly. These investments will face challenges, introspection and learning won’t be applied, and the strategy will likely be abandoned.

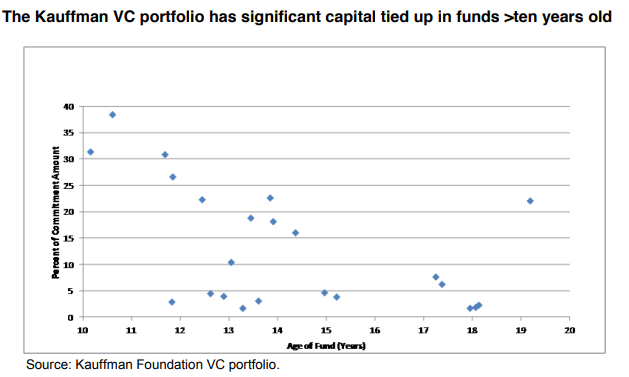

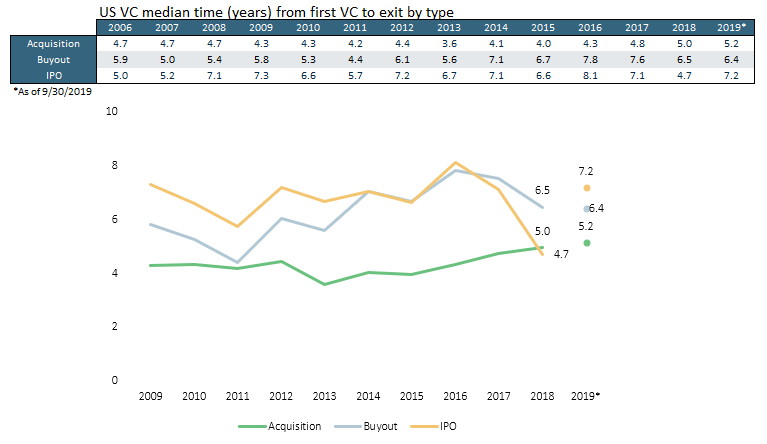

The Kauffman Foundation has a great report on venture investing examining the outcomes of investing in 88 venture funds over a period of ~20 years. Twenty-three funds were ten to fifteen years old and eight funds were fifteen years or older. That’s a long hold period. PitchBook 2019 Q3 NVCA Venture monitor data puts the average time to exit from first VC investment for 2019 exits at 6.4 years with a median of 5.5 years. PwC / CBInsights MoneyTree reports estimate the average time to exit around 6.5-7.5 years. If a FO’s venture experience is similar to this data, the feedback loop can be very long when assessing the final success or failure of the opportunity.

Your principals can become distracted or have their determination waiver without a couple of prospective winners in the early stages of building out the portfolio. Dealing with disillusionment is real when the first investment was made 4-5 years ago, there hasn’t been an exit, and maybe a couple of companies are exhibiting traction while the other investments are struggling and taking up resources from the team. New FOs can start out with a capital gains mandate only to have their principals start asking about liquidity, cash generation, etc. 2-3 years into the life of the team. I can promise your principals can find creative ways to burn money that will give them more joy with a lower level of stress and take less of the team’s energy.

Expectation: We have a great network that will help send us proprietary deals.

Reality: Most the people you know are even worse at venture investing than you are. Relying on their ideas can go poorly for everyone involved.

Great venture deals flowing through your network (unless you’re in a major venture hub connected with the right people) are more uncommon than FO principals and staff likely realize. Much of your high-powered network sees fewer opportunities than your team. The team would be well served to put effort into building out new networks that are integrated into the entrepreneurial ecosystem(s) where the FO aims to invest. Going to the accelerator up the street and attending a few demo days is a good start but won’t cut it in the long run.

Expectation: We’re not in one of the major venture hubs. We will be the go-to source of capital in our backyard, helping build an entrepreneurial ecosystem providing us with a reputation for future deals and solid returns.

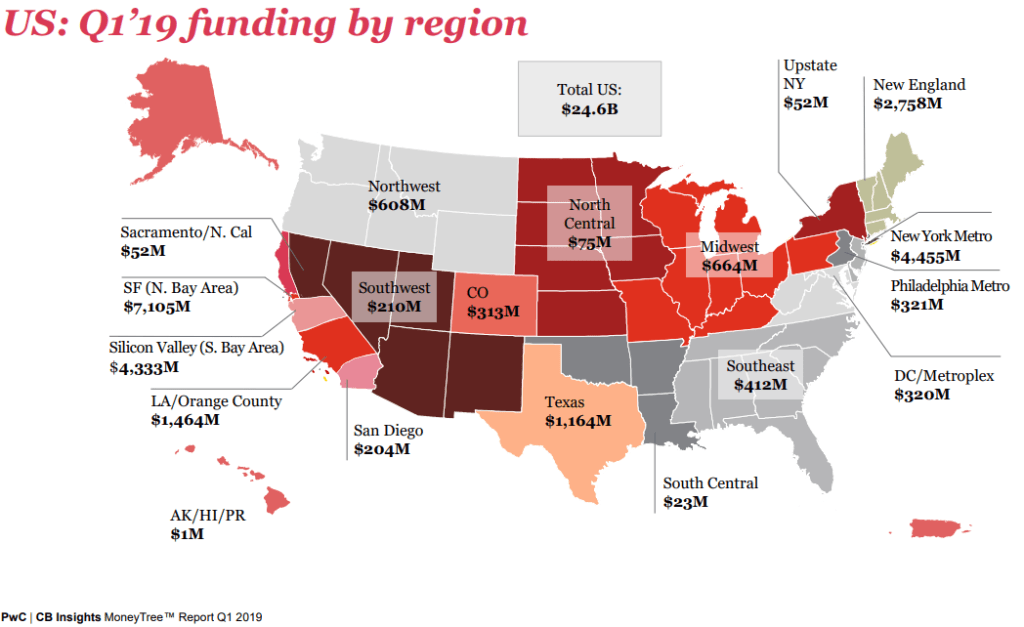

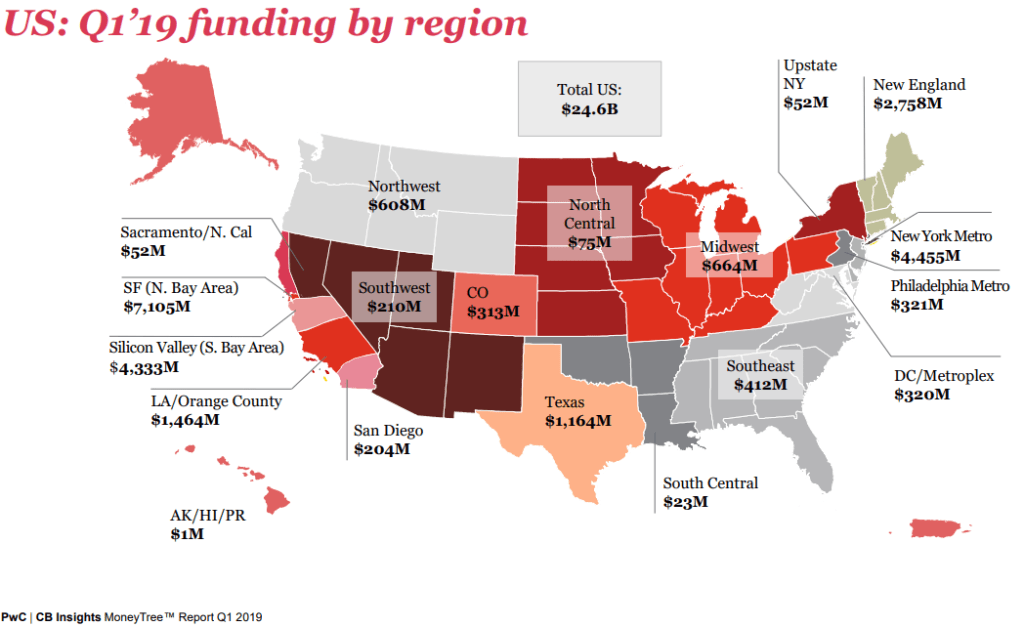

Reality: Your backyard doesn’t have enough talent at this time to merit only investing in the HQ city of the staff and family. Deals won’t be attractive or there won’t be enough activity to merit the investment of staff’s time. Let’s take a look at the PWC/CB Insights MoneyTree Report from 2019 Q1 for some context (I like the visual of the maps so I’m using older data, please check out the latest report for up to date information). Deal volume and dollars (skewed by late stage growth rounds) are still heavily weighted to the major venture hubs on the coast.

The home base for the family might not have the breadth and depth of deal volume for a staff resource to spend the majority of their time looking for ideas to deploy a relatively small amount of capital annually. The southeast region had 65 deals averaging just over $6.5M in capital per funding in the quarter in 2019 Q1. That’s a lot more work to cover relative to say the LA/Orange County region, but LA will have more known venture investors our there competing for quality deals. Maybe having a manager in town who can do the legwork for you while providing broader portfolio diversification and still helping grow your area’s ecosystem is a better way to go.

Venture investing is a topic I’m sure we’ll explore more in the future. If your team is considering a venture capital strategy, I encourage them to spend some time understanding the proposed strategy before putting significant capital to work.