This post is long overdue and was sitting mostly finished for several months. Life upheaval and burnout were impediments to delivering timely commentary on the UBS 2020 Global Family Office Report. We will cover the contents of the 2020 report, which I recommend reading if you are interested in family offices (“FOs”). All charts are from the 2020 UBS Report with one exception. This post will review structural changes between the 2019 and 2020 surveys, private investments, asset allocation, ESG/Impact/Sustainable investing, and some random data points and thoughts. For reference, my post on the 2019 report can be found here.

I aspire to be more active over the coming months as life is more settled compared to the summer.

What Changed in the 2020 Survey

Data points, perspectives, and trends relative to the two previous iterations of the UBS report may not be as applicable for the 2020 survey which had 121 participants compared to 2018 and 2019’s 311 and 260 participants, respectively. The report appears to be focused on single family offices (“SFO”) while previous incarnations included multi-family office contributors, which made up about 20% of prior survey respondents. 2020 participants averaged a reported net worth of $1.6B, which is higher than 2019 FO respondents average net worth of $1.2B and average SFO net worth of $1.3B. ~21% of 2020 survey participants declined to disclose the FO net worth. Overall the 2020 vintage provides readers with less information across the board, but we’ll make due with what is available. UBS appears to have made changes in staffing for their team covering FOs (no connections to the organization in a work capacity), which could be driving changes to the format.

Private Equity – The Hero Family Office Investors Want

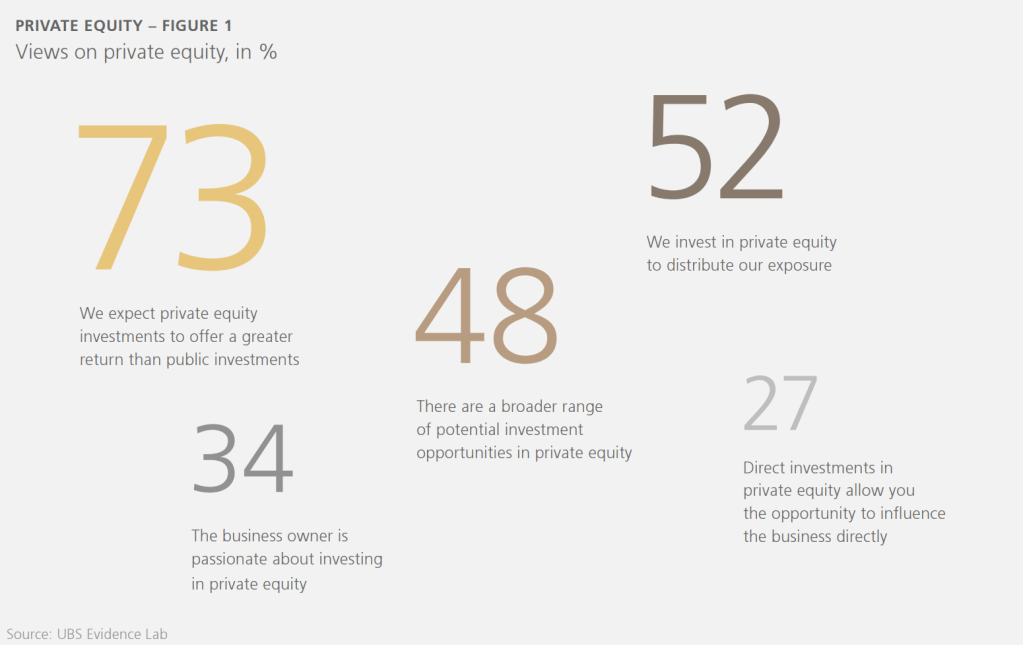

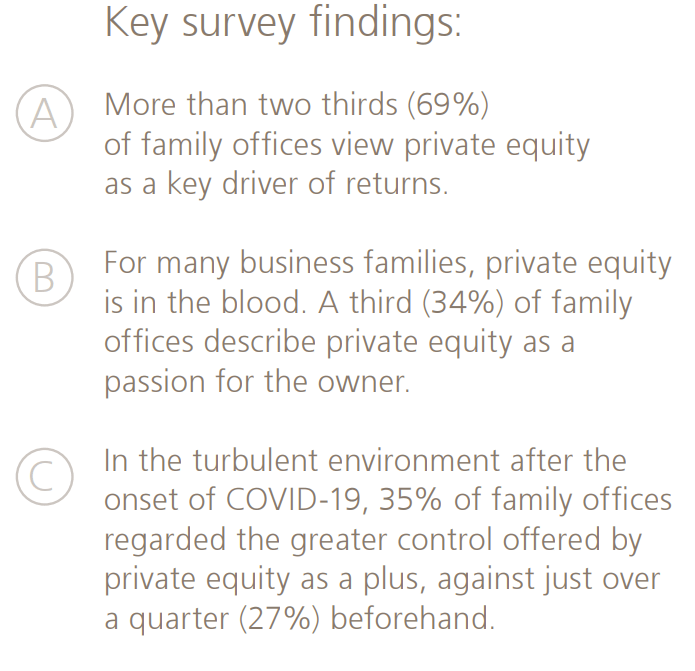

48% of FOs invest in private equity (“PE”) to access a broader range of opportunities. 69% of responding FOs view PE as a key driver of returns with 34% of FOs describing PE as a passion for the owner. 73% of FOs expect PE to deliver higher returns compared to public markets. 52% of FOs state they invest in PE for diversification purposes and the ever-important benefit of not having assets priced daily.

There are interesting nuggets on survey respondents approach to PE investing. Direct investing FOs actively investing in PE had five deals under review in the months ahead of the crisis. Depending on your interpretation of ‘under review in the months ahead’, this number could be relatively respectable or a data point highlighting deal flow challenges faced by many FOs attempting to execute direct investing strategies. The language in the report is squishy enough that I am assuming more of a negative connotation on the amount of and quality of opportunities seen by most FOs attempting to invested directly into businesses, but I have strong biases on the subject. Unsurprisingly FO owners (68%) prefer to invest in sectors with higher levels of familiarity to the office. As a practical matter, those who want to raise capital from FOs are more likely to find success pitching ideas to families with ties to that industry. Professionals considering a working for an investing FO should keep this reality top of mind when considering any potential career opportunity with a FO.

Greater control of PE investments was seen as a positive by 35% of FOs vs 27% in 2019’s survey. The perception of control provides comfort whether or not that control can be and is used to create better outcomes. I hope they’re right in assessing their abilities if FOs choose to get more involved with their investments, a journey that can burn considerable amounts of time and resources.

A striking data point for your author was 38% of FOs investing in PE had the family as the main source of new deals, which I view to be a negative for investing outcomes over the long-run in most circumstances. The family providing the majority of deal flow is likely to anchor expectations for the organization regarding the quality and filter types of ideas seen by the organization. Principals lacking meaningful deal experience driving the opportunity set for the team is likely to create challenges due to a lack of understanding of what constitutes a quality deal by the individual(s) controlling the deal funnel. Many principals believe they have a stronger network for sourcing investment ideas than the reality of the situation. At the end of the day the capital belongs to the principals and they have final say over what happens, but a narrow approach on partners and deal sources can produce negative outcomes for the organization over time.

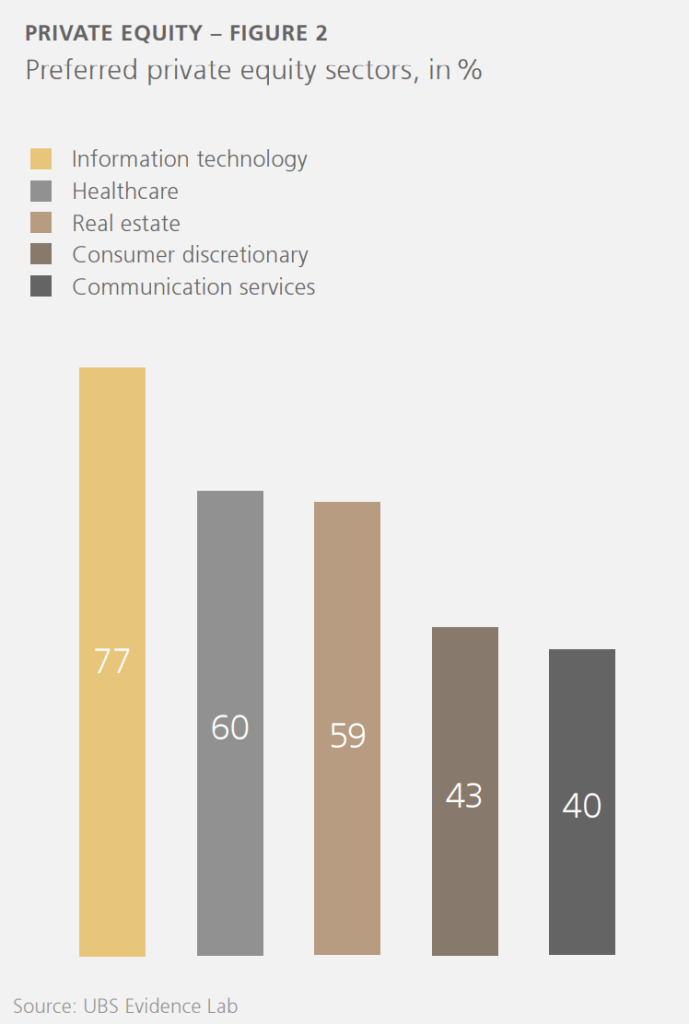

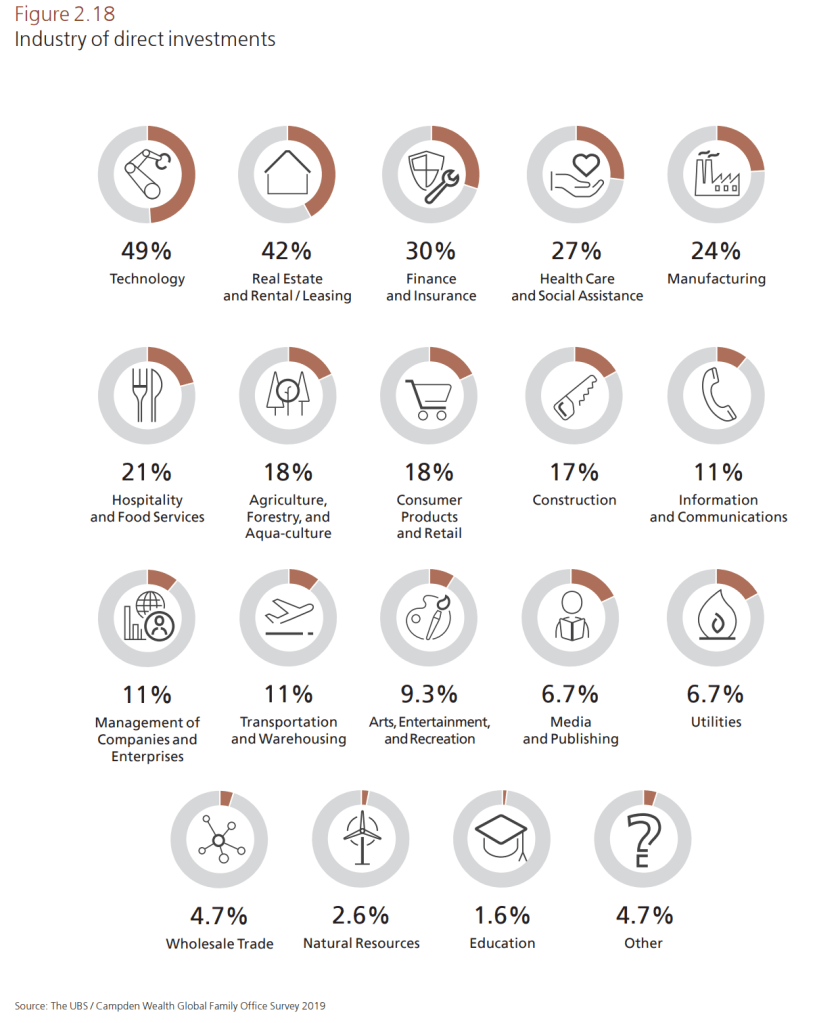

The two charts below aren’t apples to apples because the 2019 information refers specifically to direct investments while 2020 refers to private equity sectors generally, but technology, healthcare, and real estate remain popular sectors for FO investment activity. Assuming the data sets correlate, 2020 survey participants saw a material increase in the desire to invest in healthcare focused investments with health care being the second most popular sector for FO PE investments. Healthcare was the fourth most popular direct investment sector for 2019 FO survey responders. Consumer discretionary is also a sector potentially generating more interest between the two surveys. The survey notes that FO usually diversify across four or five sectors for their PE investments.

Private Investments – Other Items of Note

- Both cohorts preferred to make growth equity investments with 70% and 71% of 2019 and 2020 respondents making growth investments.

- Ventures was marginally less popular in 2020 with 53% of FOs investing compared to 57% in 2019.

- LBO investments weren’t as common in the 2020 cohort with 40% of FOs investing in LBOs compared to 55% in 2019. Surprising to me considering the 2020 group had larger AUM and buyout funds seem to get more traction with larger groups relative to smaller FOs in my experience.

Asset Allocation

Given the timing of this post lagging the source material, I’ll keep the asset allocation observations high level and quick.

- 76% of FOs reported their portfolios performed in-line with or above their respective target benchmarks over the year to May.

- 13% max drawdown on average of survey respondents.

- 2/3s were trading up to 15% of their portfolios tactically during the early stages of COVID. 55% rebalanced.

- Respondents had relatively more exposure to developing markets in their fixed income allocations when compared to their equity allocations.

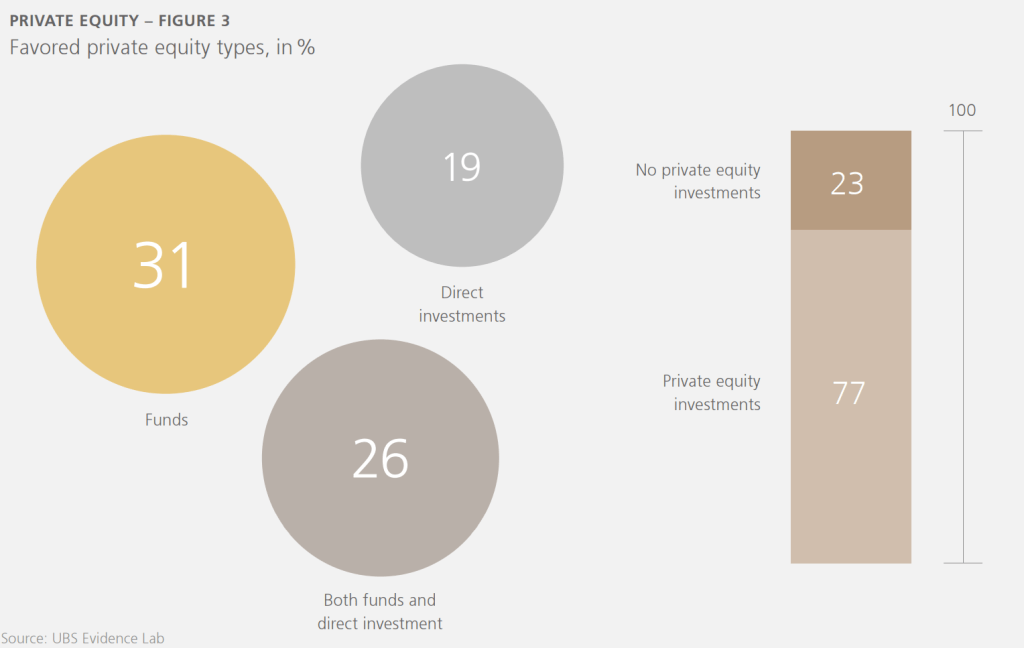

- Private equity allocations were ~56% direct investments and ~44% funds.

- Principals are the main driver of strategic asset allocation for 28% of respondents and another 28% of respondents have principals that share the asset allocation responsibilities with investment staff.

- Responding FOs expect to invest from elevated cash positions over the next two to three years with real estate as the asset class expected to see the most new investment followed by direct private equity.

- 45% of respondents expect to raise allocations to real estate in the coming years. Based on my experiences, real estate is the asset class that has the most success and lowest level of difficulty in raising capital from FOs.

- Not meeting investment goals was the number one risk to manage.

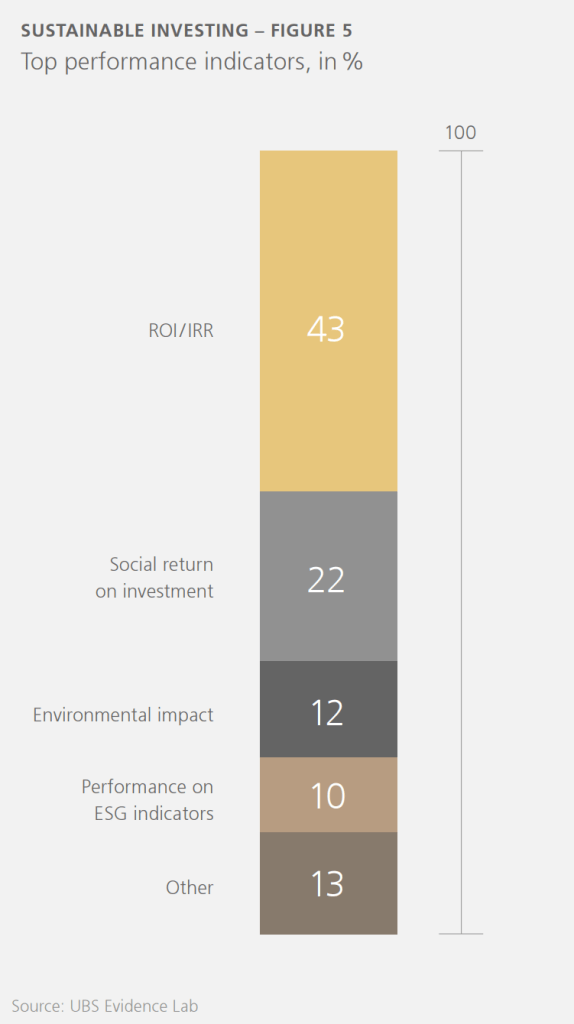

ESG/Sustainability/Impact – Wave of the Future?

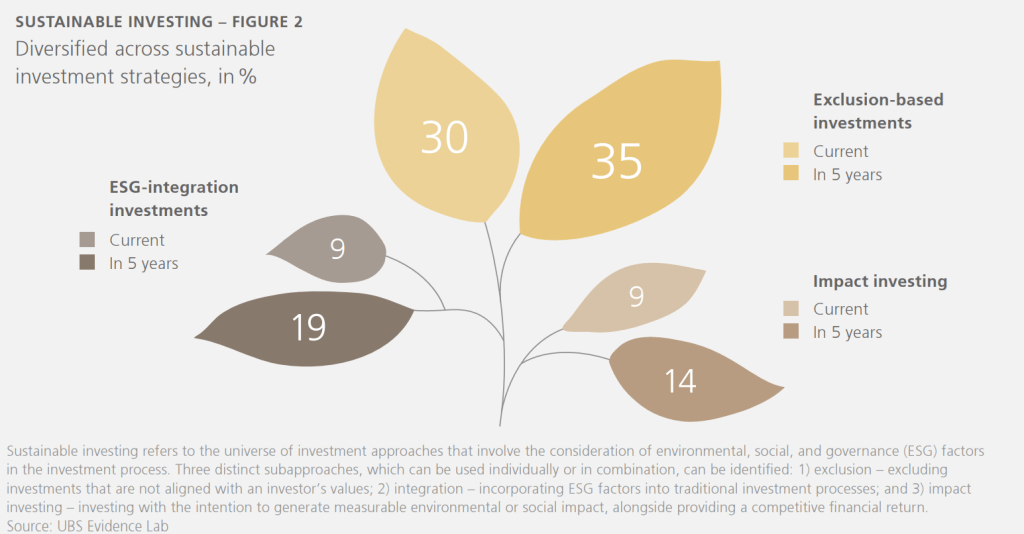

Sustainable, ESG, or Impact investing continues to be a space of interest for global FOs. Personal experience and comments in various iterations of the USB surveys reinforce the idea that measuring or defining impact remains a challenge for FO investors. Exclusion style investing was the most popular expression of sustainable investing for 2020 survey participants while a smaller subset are actively making ESG and impact styled investments. The general expectation was for increased activity in all three styles over the next five years. Groups that are successful at framing or defining impact could find some FOs welcoming them as new partners.

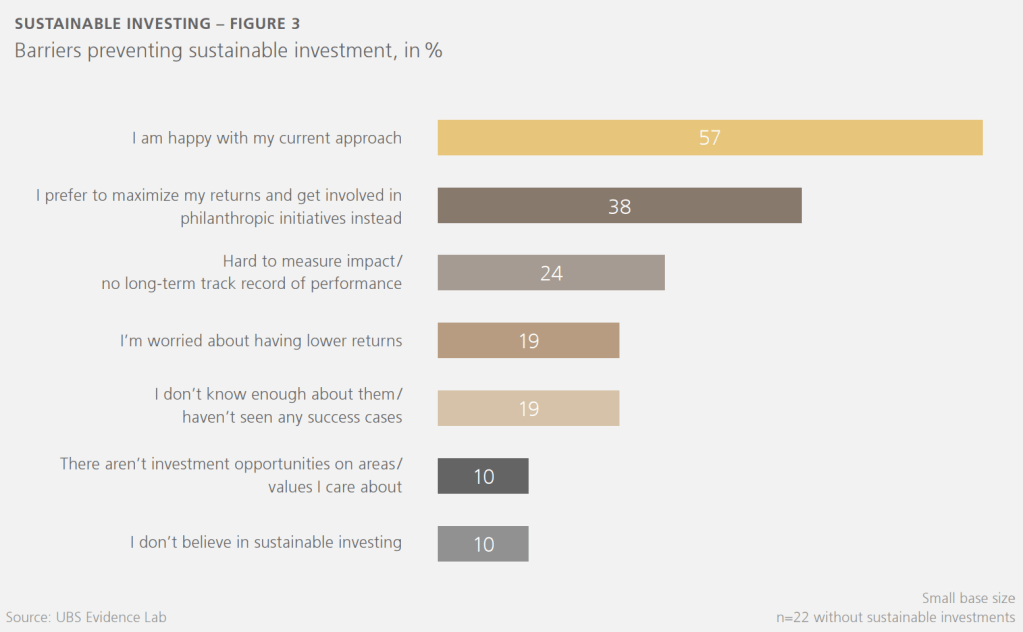

Follow through about Sustainable/Impact/ESG by FOs remains a question mark. Survey responses lay out barriers or concerns for adopting sustainable investing. Maximizing returns and being more involved philanthropically was seen as more attractive to 38% of responding FOs.

Finally, a different kind of green continues to be the biggest driver of any potential green investments. I remain skeptical about the staying power of ESG/Impact investing as structured today unless there are businesses that can deliver impact and high levels of return.

Additional Thoughts

- ~1/3 of FOs had no plans for a change in control despite most beneficial owners being in their 60s and 70s. Might be time for some organizations to be putting a plan in place.

- ~56% of families remain closely involved in strategic asset allocation. People are always looking to get direct access to the family with a belief that talking to a family member will improve the chances of that individual or team getting a desired outcome with the FO (mostly raising money). Those that are lucky enough to have a conversation or email exchange with a principal about their investment opportunity are likely to find the family’s level of interest disappointing.

- 70% of FOs have their own research team to evaluate investment opportunities. Couldn’t give any context on how representative the data point is of reality, but found the number interesting.

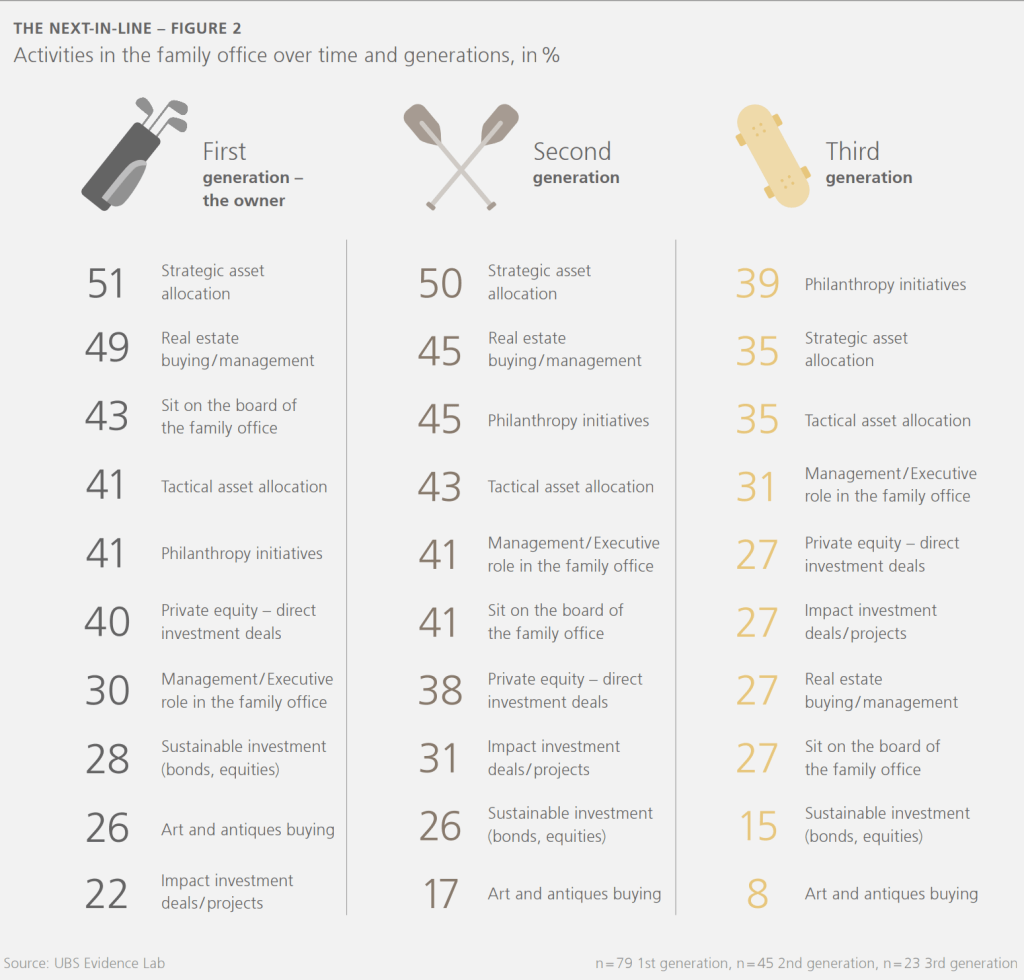

- Good chart below showing the difference in interests by generation. The generation of the principals can be a key insight into how a particular FO might handle their business.